When Crypto Came Onchain: The Mainstream Moment

When Crypto Came Onchain: State of Market 2025

Three years can transform an industry beyond recognition. When a16z published their first State of Crypto report, blockchain technology remained firmly in its experimental phase. Networks crawled under the weight of transactions, fees ran astronomically high, and most people viewed cryptocurrency as either a speculative curiosity or an outright scam. Fast forward to 2025, and the landscape has shifted so dramatically that the change feels less like evolution and more like revolution.

The total crypto market capitalization crossed the $4 trillion threshold for the first time this year. That number alone tells an important story, but the real narrative lies deeper in how this technology has woven itself into the fabric of mainstream finance and everyday transactions. This isn't about another price milestone or another all-time high. This marks the moment when crypto stopped being an alternative system and started becoming simply another way people interact with money.

The Numbers That Tell a Transformation Story

Consider the user growth patterns emerging from recent data. Somewhere between 40 and 70 million people now actively transact on blockchain networks monthly, representing an increase of approximately 10 million users over the past year. These aren't just holders or speculators. These are individuals conducting real transactions, moving value, and engaging with decentralized applications on a regular basis.

The gap between these active users and the 716 million global crypto owners reveals something fascinating about the current state of adoption. While ownership has expanded significantly (up 16% from last year), the percentage of owners who regularly transact onchain remains relatively small. This distance between passive holders and active participants represents enormous untapped potential. As more users discover practical applications for their digital assets beyond simple holding, that gap should narrow considerably.

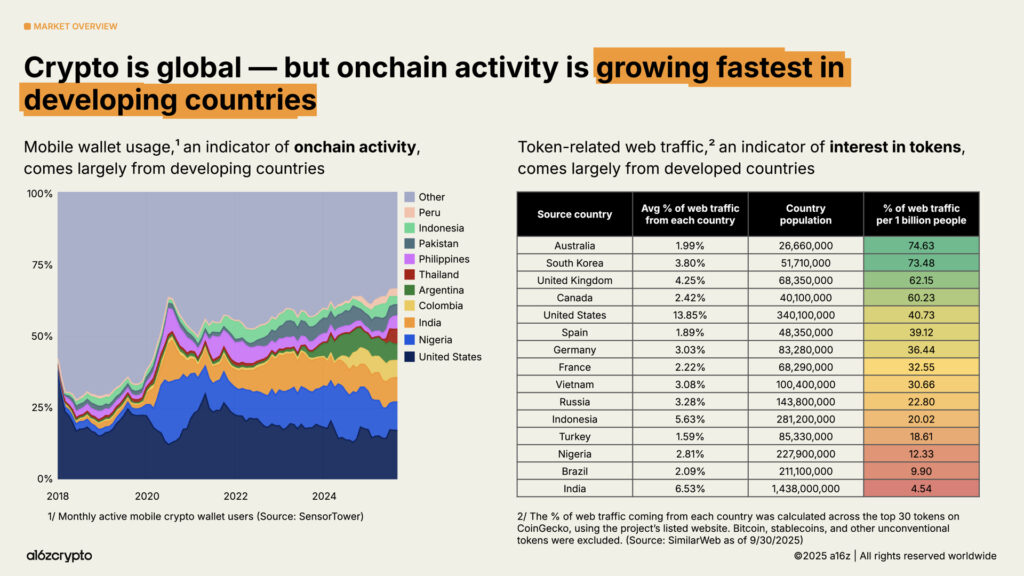

Geographic patterns in usage reveal interesting distinctions about how different regions engage with crypto technology. Mobile wallet usage, which serves as a reliable indicator of onchain activity, is growing fastest in emerging markets across Argentina, Colombia, India, and Nigeria. These regions have seen consistent increases in crypto mobile wallet adoption over the past three years, often driven by currency instability or limited access to traditional banking infrastructure.

Meanwhile, interest in tokens skews toward developed nations. Analysis of geographic sources for token-related web traffic shows activity concentrated in countries like Australia and South Korea, with substantially higher per-capita engagement compared to developing countries. This suggests different use cases emerging along economic lines: emerging markets gravitating toward practical payment and remittance solutions, while developed economies focus more on trading and speculation.

Bitcoin continues its dominance within the crypto ecosystem, representing more than half of total market capitalization even as its share has gradually declined from peaks above 70%. Ethereum and Solana have steadily captured market share, driven largely by the explosion of decentralized applications and smart contract platforms. As blockchains continue scaling and new applications emerge, certain metrics beyond simple market cap are becoming increasingly important. Real economic value, measured by the actual fees people pay to use various blockchains, tells a more nuanced story. Today, Hyperliquid and Solana account for 53% of revenue-generating economic activity, marking a significant departure from Bitcoin and Ethereum's historical dominance.

The Stablecoin Revolution

Perhaps no development in 2025 signals crypto's mainstream arrival more clearly than the explosive growth of stablecoins. These digital currencies, pegged to traditional assets like the US dollar, have become the fastest, cheapest, and most global way to send value. In years past, stablecoins served primarily to facilitate crypto trading, offering traders a way to move quickly between positions without converting back to fiat currency. That utility remains, but it now represents only one piece of a much larger picture.

Stablecoins processed $46 trillion in total transaction volume over the past year, up 106% from the previous year. On an adjusted basis that filters out artificial activity like bot transactions, genuine user-driven stablecoin activity reached approximately $9 trillion in the last 12 months, up 87% year over year. These figures rival those of traditional payment networks. Visa processes roughly $16 trillion annually, while PayPal handles about $1.7 trillion. Stablecoins now sit firmly in that same competitive tier.

The shift from trading tool to payment infrastructure reflects stablecoins' growing utility for real-world transactions. People use them to send remittances across borders in seconds rather than days, to make purchases from merchants increasingly comfortable accepting digital payments, and to preserve value in regions experiencing currency volatility. Monthly adjusted stablecoin transaction volume reached all-time highs approaching $1.25 trillion in September 2025 alone.

The total stablecoin supply now exceeds $300 billion, representing over 1% of all US dollars currently in existence as tokenized versions on public blockchains. This presents both an opportunity and a challenge for the US dollar's global position. Stablecoins could strengthen dollar dominance as foreign central banks reduce their Treasury holdings. Foreign demand for US debt has waned significantly (US Treasuries represent about 20% of foreign reserves today, down from peaks above 30% in previous decades, while gold holdings have increased). Stablecoins denominated in USD and projected to grow 5-10x to over $3 trillion by 2030 represent a potentially strong and sustainable new source of demand for US debt.

Tether and USDC dominate today's stablecoin supply, accounting for 87% of the total market and settling $772 billion in transactions (adjusted) on Ethereum and Tron blockchains in September 2025 alone. This represents 64% of all transaction volume. While these two issuers and chains handle the bulk of activity, growth among new chains and issuers continues gaining momentum.

More significantly, stablecoins have already become a top 20 holder of US Treasuries, positioning ahead of countries like Saudi Arabia, South Korea, Israel, and Germany. This ranking will likely continue rising as stablecoin supply expands. Over 99% of stablecoins are denominated in USD, and they're projected to grow substantially. Even as foreign central banks reduce their dollar holdings, stablecoins are strengthening dollar dominance through an entirely new mechanism.

Financial Institutions Join the Movement

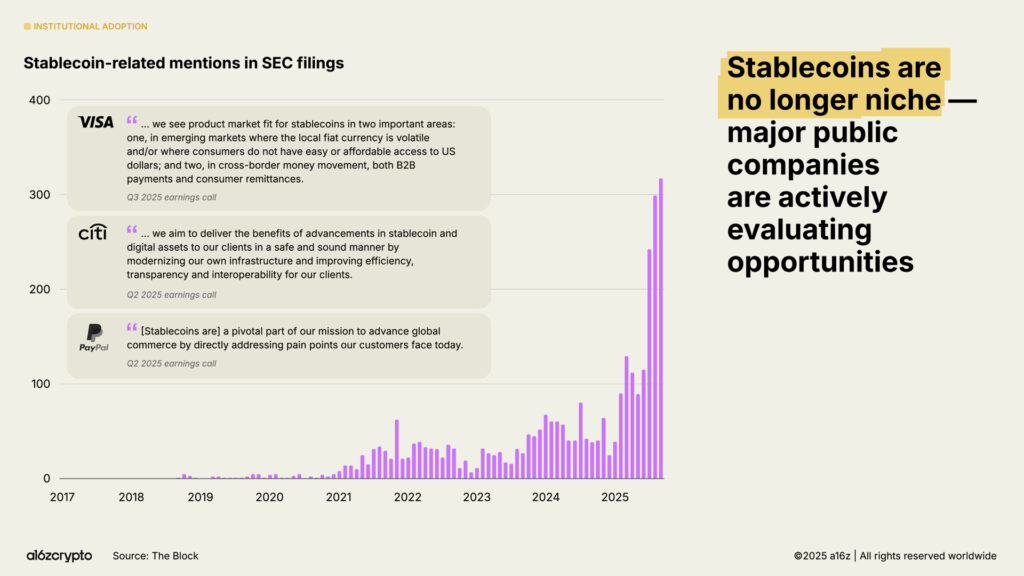

The stablecoin story connects directly to another major 2025 theme: institutional adoption. Traditional financial institutions have moved decisively into crypto over the past year, transforming what was once a fringe experiment into a core component of modern financial infrastructure.

Just five days after announcing stablecoins had found product-market fit in last year's State of Crypto report, Stripe revealed its intent to acquire stablecoin infrastructure platform Bridge. The race had begun. Traditional finance companies shifted from cautious observation to active participation seemingly overnight. Major institutions including Citigroup, Fidelity, JPMorgan, Mastercard, Morgan Stanley, and Visa now offer (or are planning to offer) crypto products directly to consumers, allowing them to buy, sell, and hold digital assets alongside equities, exchange-traded products, and other traditional instruments.

Beyond direct offerings, major fintechs are building or acquiring blockchain infrastructure. Stripe acquired Bridge and launched wallet infrastructure company Privy, then announced a new payments-focused blockchain called Tempo. Circle, Robinhood, and Stripe are actively developing or have announced plans to develop new blockchains focusing on payments, real-world assets, and stablecoins. These initiatives signal that traditional finance sees blockchain not merely as another asset class but as fundamental infrastructure for the financial system's next iteration.

Exchange-traded products represent another key driver of institutional investment, with over $175 billion now flowing into onchain crypto holdings through Bitcoin and Ethereum ETPs. These products have grown 169% from $65 billion just a year ago. BlackRock's iShares Bitcoin Trust achieved remarkable milestones as the world's fastest ETP to reach $10 billion, $25 billion, and $50 billion in assets under management.

Publicly traded digital asset treasury companies now collectively hold about 4% of the total Bitcoin and Ethereum in circulation. Combined with exchange-traded products, these vehicles now control approximately 10% of both Bitcoin's and Ethereum's token supplies. This represents a fundamental shift in how institutional capital accesses crypto markets, moving from direct purchases on exchanges to regulated investment vehicles that fit within traditional portfolio management frameworks.

Regulatory Clarity Transforms the Landscape

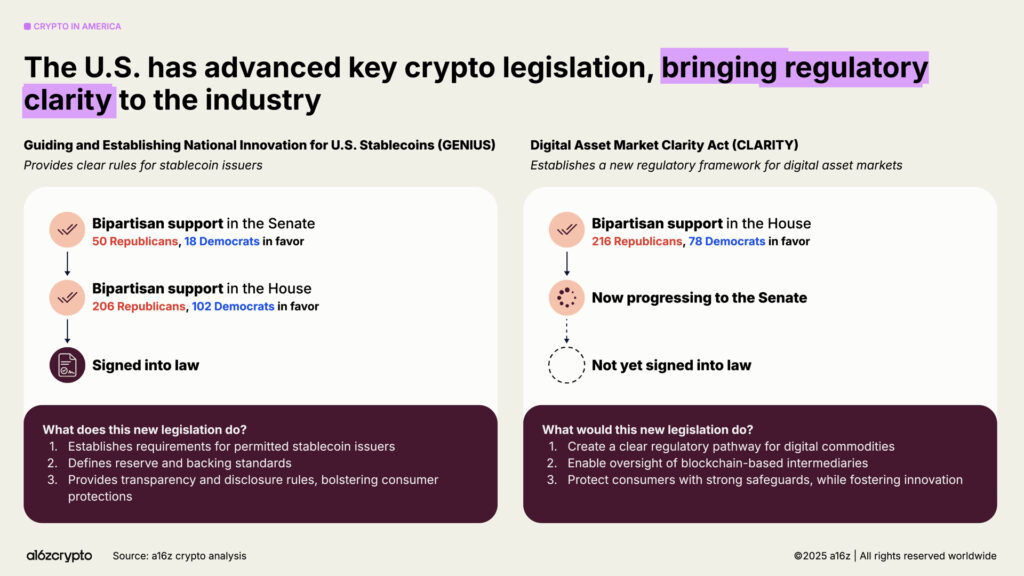

Institutional adoption accelerated in part because regulatory clarity finally began emerging after years of uncertainty. The United States has reversed its formerly antagonistic stance toward crypto, reviving builder confidence through concrete legislative action.

The passage of the GENIUS Act and House approval of the CLARITY Act in 2025 signal a bipartisan consensus that crypto deserves a place in America's financial future. These bills establish frameworks for stablecoins, market structure, and digital asset oversight that balance innovation with investor protection. The legislation was complemented by Executive Order 14178, which reversed earlier anti-crypto directives and created a cross-agency task force to modernize federal digital-asset policy.

The regulatory environment has created pathways for network tokens to complete their economic loop by generating revenue that accrues directly to tokenholders. With regulatory clarity, more network tokens can function as intended, creating self-sustaining economic engines for the internet. Crypto users paid $33 billion in fees over the last year. A significant portion of that (approximately $18 billion based on recent data) now flows directly back to crypto projects as revenue, enabling them to fund development, reward participants, and build sustainable ecosystems.

This completes a critical feedback loop. Users pay for services. Those payments generate revenue for networks. Networks use that revenue to improve services and reward stakeholders. More users arrive attracted by better services. The cycle continues, creating network effects similar to what made previous generations of internet platforms successful, but with a crucial difference: value accrues to a broader base of participants rather than concentrating within a single corporate entity.

The Onchain Economy Emerges

What happens when tens of millions of people can transact freely on global networks with negligible fees? A new economy emerges, one that looks quite different from the speculation-heavy environment of crypto's early years.

The onchain economy now resembles a multi-sector marketplace with tens of millions of monthly participants. Nearly one-fifth of all spot trading volume now flows through decentralized exchanges rather than centralized platforms. Perpetual futures, a sophisticated crypto product that became mainstream during the last cycle, exploded among crypto speculators. Decentralized perps exchanges like Hyperliquid have processed trillions of dollars in trades and generated more than $1 billion in annualized revenue this year, numbers that rival some centralized exchanges.

Real-world assets are bridging traditional finance and crypto, with $30 billion already onchain. These tokenized versions of traditional assets like US Treasuries, money-market funds, private credit, and real estate represent just the beginning. The total market for such assets sits at roughly $30 billion today, up nearly 4x in the last two years. Major blockchains hosting RWAs include Ethereum, ZKsync Era, Polygon, Arbitrum, Avalanche, Aptos, Solana, BNB Chain, Stellar, and XRP Ledger.

Decentralized physical infrastructure networks represent one of the most ambitious frontiers for blockchains in 2025. DePIN projects reimagine physical infrastructure including telecom and transportation networks, energy grids, and more. The opportunity is substantial. The World Economic Forum projects the DePIN category will grow to $3.5 trillion by 2028. The Helium network exemplifies this potential. This grassroots wireless network now provides 5G cellular coverage to 1.4 million daily active users across more than 111,000 user-operated hotspots.

Prediction markets broke into the mainstream during the 2024 US presidential election cycle, with platforms like Polymarket and Kalshi seeing billions in combined monthly trading volume. Despite initial skepticism about whether these platforms could sustain engagement outside election years, trading volume has increased nearly 5x since the start of 2025, nearing previous highs. This suggests prediction markets have found lasting product-market fit as a form of information aggregation and speculative entertainment.

Infrastructure Reaches Critical Mass

None of this activity would be possible without the dramatic infrastructure improvements blockchain networks achieved over the past five years. In just five years, aggregate transaction throughput across major blockchain networks increased more than 100x. Blockchains processed fewer than 25 transactions per second in 2020. Now they process approximately 3,400 transactions per second, approaching the scale of some of the largest financial systems. For comparison, Stripe processes roughly 2,300 transactions per second during peak periods like Black Friday and Cyber Monday, while Nasdaq handles approximately 2,400 trades during open hours.

Ethereum's scaling roadmap continues delivering results, with most economic activity migrating to Layer 2 networks such as Arbitrum, Base, and Optimism. Average transaction costs on these L2s have dropped from around $24 in 2021 to less than one cent today, making Ethereum-linked blockspace cheap and abundant. Recently, upgrades accelerated blockchain activity and drove throughput through all-time highs, with Ethereum and its L2s processing 236 transactions per second in September 2025.

Solana has emerged as a hub for onchain economic activity with rising throughput, ultra-cheap fees (averaging less than half a cent), and billions in application revenue. The network's high-performance, low-fee architecture now underpins everything from DePIN projects to NFT marketplaces, with native applications generating $3 billion in revenue in the past year. Planned network upgrades are expected to double capacity by year-end.

Billions of dollars now flow between blockchains as interoperability infrastructure becomes more robust. Bridges are allowing blockchains to interoperate, with protocols like LayerZero and Circle's Cross-Chain Transfer Protocol enabling users to move assets across a multichain system. Hyperliquid's canonical bridge reached $74 billion in volume year to date, demonstrating the scale these cross-chain solutions have achieved.

Privacy Technologies Mature

As crypto reaches more mainstream users, privacy concerns have intensified. The need for privacy has grown more urgent than ever. Privacy-related Google searches surged in 2025, Zcash's shielded pool supply grew to nearly 4 million ZEC, and Railgun's transaction flows surpassed $200 million monthly.

Zero-knowledge proofs have become critical to blockchain privacy and scalability, fueling rapid acceleration in technical progress. These cryptographic techniques allow one party to prove to another that a statement is true without revealing any information beyond the validity of the statement itself. The development timeline of ZK technology shows remarkable progress from theoretical foundations in the 1980s to practical implementations today. Recent innovations in transparent polynomial commitments and universal SNARKs are exploring universal setups, linear-time provers, and lookup optimizations.

At the same time, blockchains are preparing for the transition to quantum-secure cryptography. Roughly $750 billion in bitcoin sits in addresses vulnerable to future quantum attacks. The US government plans to transition federal systems to post-quantum cryptographic algorithms by 2035. The Bitcoin community has proposed an upgrade for post-quantum security, while Ethereum co-founder Vitalik Buterin has proposed quantum-resistant signature schemes.

More signs of momentum continue emerging. The Ethereum Foundation formed a new privacy team, Paxos partnered with Aleo to launch a private, compliant stablecoin, the Zcash wallet Zashi integrated with Near Intent's cross-chain swaps, and Noir (a ZK programming language used for privacy) saw an uptick in developer activity. The Office of Foreign Assets Control officially lifted sanctions on Tornado Cash, a decentralized privacy protocol it had blacklisted in 2022.

Zero-knowledge systems and succinct proof protocols are rapidly evolving from decades-old academic constructs into critical infrastructure. Compliance tools and zero-knowledge technologies are now integrated across rollups, applications, and even mainstream web services.

The Convergence with AI

Among other advancements, the launch of ChatGPT in 2022 brought AI to the forefront of public attention, creating both opportunities and challenges for crypto. From tracking provenance and IP licensing to providing payment rails for emerging AI systems and countering AI's centralizing forces, crypto technologies offer solutions to some of AI's most pressing challenges.

It's becoming much harder to tell the difference between AI and human-generated activity online. Decentralized identity systems like World, which has verified more than 17 million people, can provide proof of personhood and help differentiate people from bots. Protocol standards such as ERC-402 are emerging as a potential financial backbone for autonomous AI agents, helping them make micro-transactions, access APIs, and settle payments without intermediaries. An economy that Gartner estimates could reach $30 trillion by 2030.

AI runs on intellectual property, but today's systems for coordinating and transacting intellectual property don't scale. Blockchains can help track provenance and facilitate IP licensing. Intellectual property assets are estimated at $80 trillion globally. AI is increasingly concentrating power among a few big tech companies. Just two companies (OpenAI and Anthropic) control 88% of "AI-native" company revenue. Amazon, Microsoft, and Google control 63% of the cloud infrastructure market, while NVIDIA holds 94% of the data center GPU market. These imbalances have fueled double-digit quarterly net income growth for the "Magnificent 7" tech giants, while earnings growth for the remaining S&P 493 companies has struggled to outpace inflation.

Blockchains offer a counterbalance to the apparent centralizing forces of AI systems. More than 420,000 GPUs have been trained on decentralized compute networks, providing alternatives to concentrated cloud infrastructure.

Amid the AI excitement, some builders have pivoted away from crypto. Analysis suggests approximately 1,000 jobs shifted from crypto to AI since the launch of ChatGPT. However, this number has been offset by an equivalent number of builders joining crypto from other areas like traditional finance and tech. The net effect appears relatively neutral, suggesting crypto's builder ecosystem remains resilient despite competition for talent from the AI sector.

Looking Forward

Where does this momentum lead? With greater regulatory clarity on the horizon, a path is clearing for tokens to generate real revenue via fees. Traditional finance and fintech adoption of crypto will continue accelerating. Stablecoins will upgrade legacy systems and democratize financial access globally. New consumer products will drive mainstream adoption onchain.

The infrastructure exists. The distribution channels are opening. Regulatory frameworks are providing clarity. The technology has matured to handle mainstream scale at costs that make practical applications viable. Seventeen years after Bitcoin's creation, crypto is finally ready to deliver on its original promise: upgrading the financial system, rebuilding global payment rails, and creating an internet economy that serves everyone with access to a smartphone.

The adolescent years are over. Crypto has entered adulthood.

Exploring how blockchain technology and digital currencies are reshaping finance and creating new economic opportunities? Our team stays at the forefront of these transformative developments. Contact us to discover how these innovations could enhance your business strategy.

References: State of Crypto 2025: a16z crypto